Crafting a robust business plan is a foundational step for any aspiring entrepreneur or growing company, and at the heart of its financial section lies the often-intimidating balance sheet. A well-constructed Business Plan Balance Sheet Template is not merely a formality for investors or lenders; it is a critical diagnostic tool that provides a clear, concise snapshot of your company's financial health at a specific moment in time. It lays bare what your company owns, what it owes, and the equity stakeholders hold, creating a framework for strategic decision-making and sustainable growth.

Understanding this financial statement is fundamental to speaking the language of business. The balance sheet operates on a simple but powerful principle: the accounting equation. This formula, Assets = Liabilities + Owner's Equity, ensures that the document is always "in balance." It's a system of checks and balances that presents a holistic view of your company's resources and obligations. By mastering its components, you move from simply filling in numbers to truly comprehending the financial structure of your enterprise.

This guide will demystify the balance sheet, transforming it from a complex accounting document into an accessible and powerful tool for your business plan. We will break down each core component—assets, liabilities, and equity—into understandable parts. You will learn not only how to populate a template accurately but also how to interpret the data to gain valuable insights into your company's liquidity, solvency, and overall stability. Whether you're a startup founder seeking seed funding or an established business owner planning for expansion, mastering your balance sheet is a non-negotiable step toward financial clarity and success.

What is a Balance Sheet and Why is it Crucial for Your Business Plan?

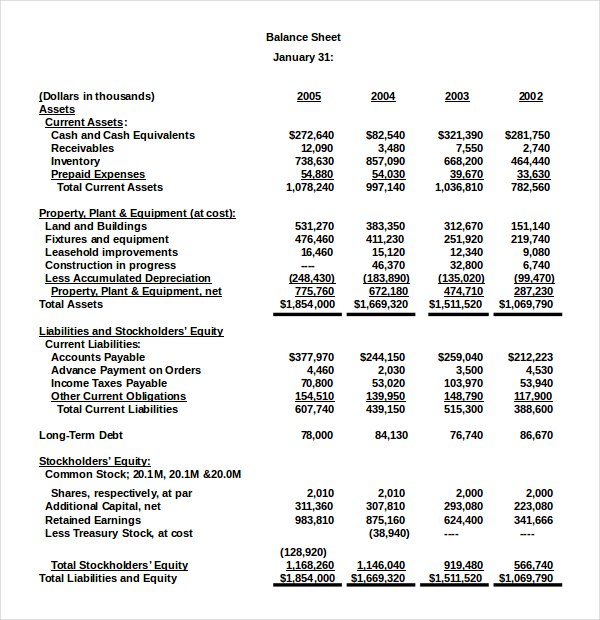

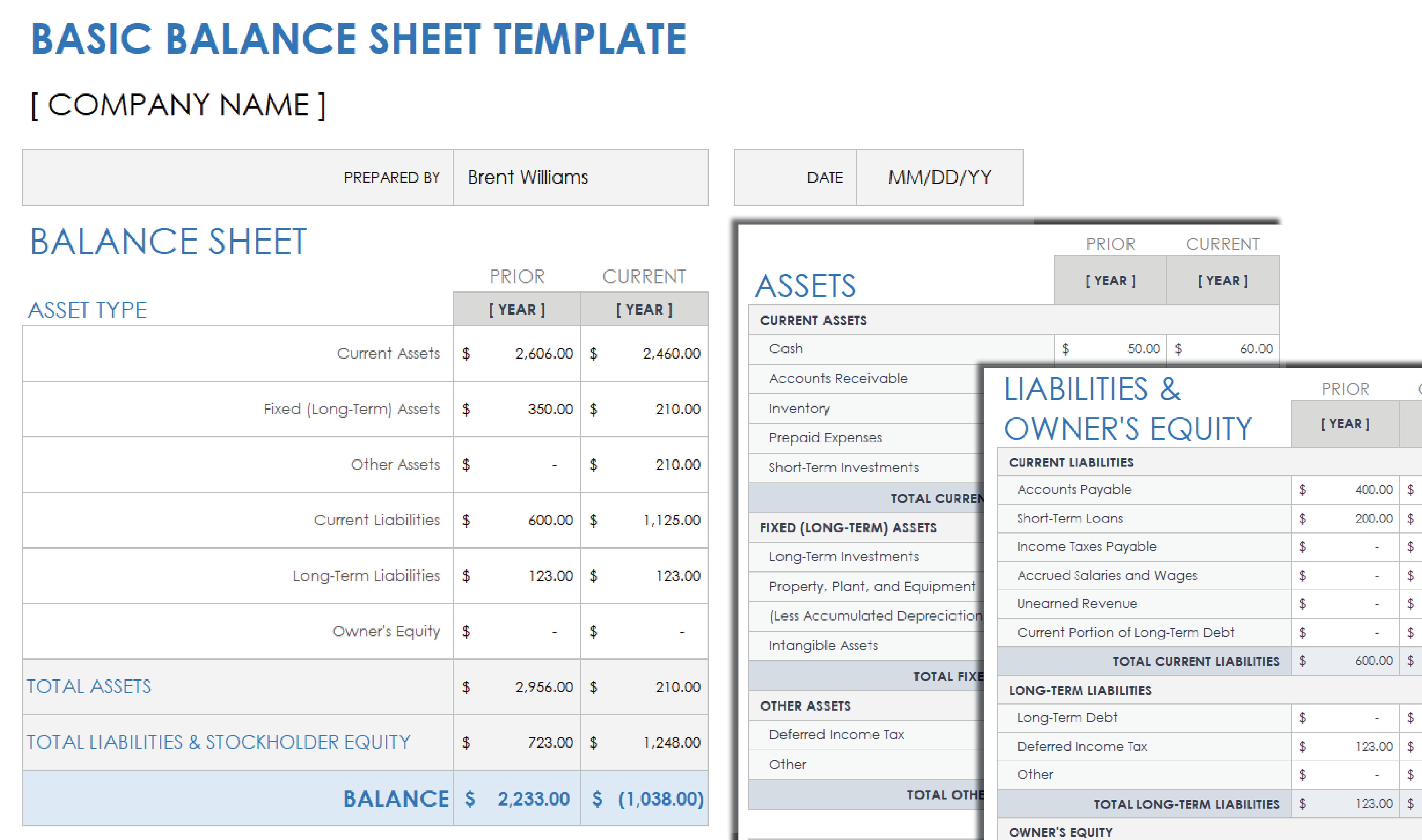

A balance sheet is one of the three core financial statements, alongside the income statement and the cash flow statement, that form the financial backbone of your business plan. Often described as a "snapshot in time," it presents a detailed picture of your company's financial position on a specific date, such as the end of a quarter or fiscal year. Unlike the income statement, which shows performance over a period, the balance sheet is static, capturing the cumulative result of all business transactions up to that point.

The entire structure of the balance sheet is built upon the fundamental accounting equation: Assets = Liabilities + Owner's Equity. This equation must always hold true. In simple terms, it means that everything the company owns (its assets) has been financed by either borrowing money (liabilities) or through investments from its owners (equity). This simple formula provides a powerful check for accuracy and a clear framework for understanding your company's capital structure.

For your business plan, the balance sheet serves several critical functions. First, for external stakeholders like investors and lenders, it demonstrates the financial stability and net worth of your company. They will scrutinize it to assess risk, evaluate how leveraged the business is, and determine its ability to meet financial obligations. A well-prepared balance sheet signals professionalism and financial competence. Second, for internal management, it is an indispensable tool for strategic planning. It helps you track debt levels, manage assets efficiently, and make informed decisions about financing, investments, and operational adjustments.

The Core Components of a Balance Sheet Explained

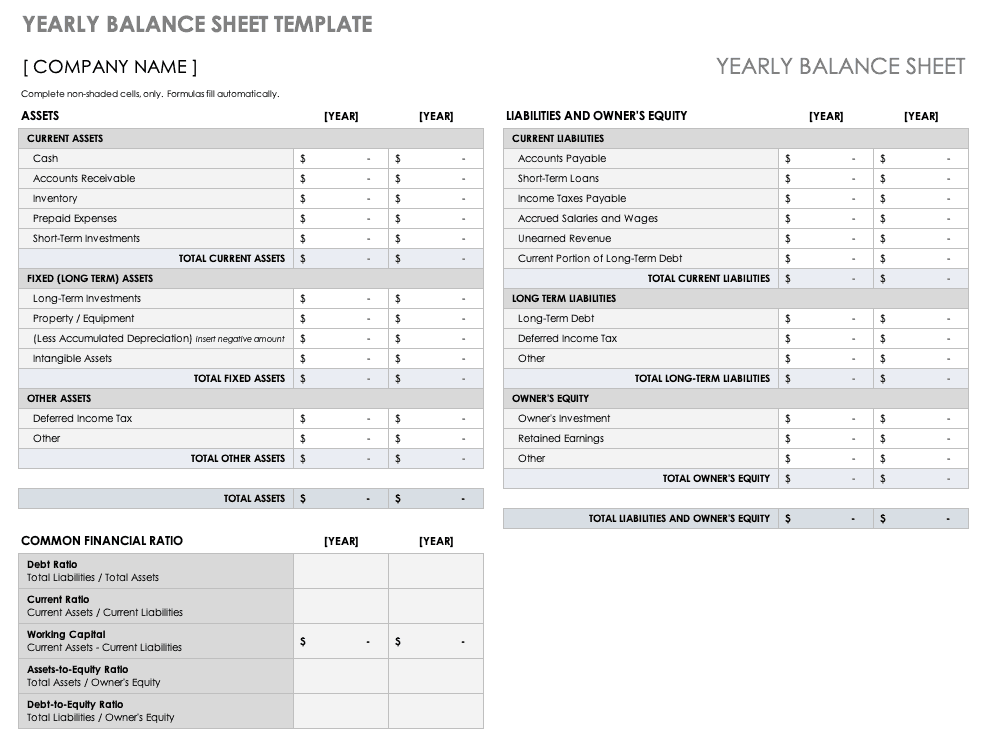

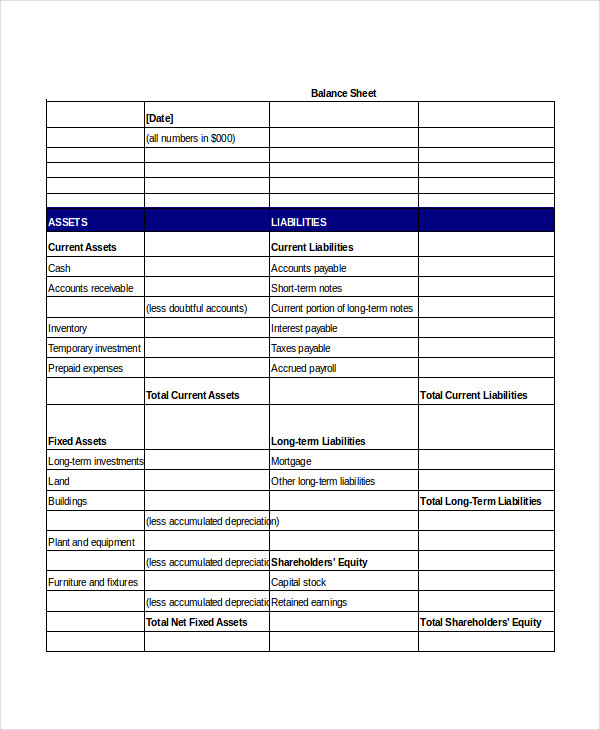

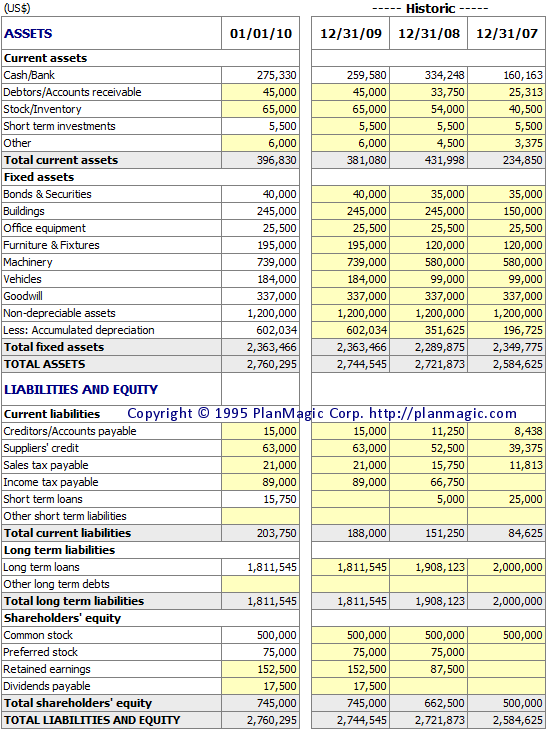

To effectively use a template, you must first understand its three primary sections: Assets, Liabilities, and Owner's Equity. Breaking these down reveals the intricate details of your company's financial story.

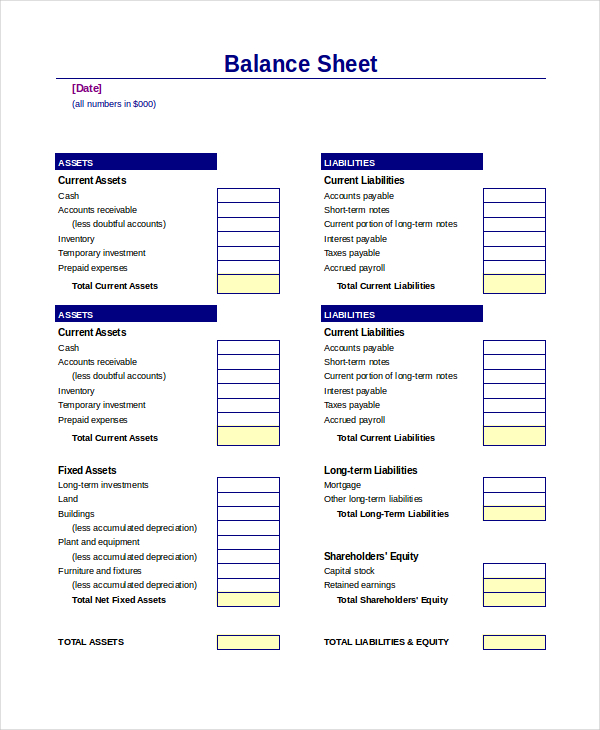

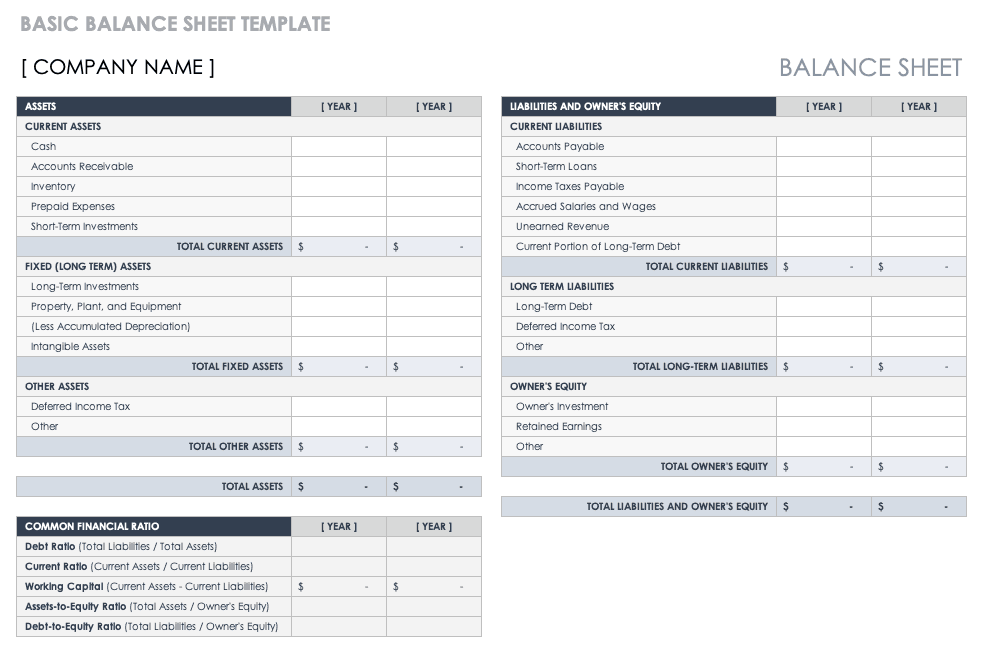

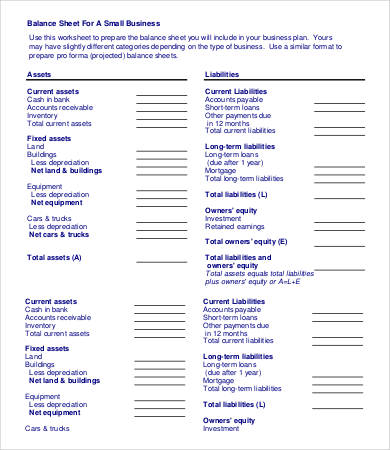

Assets: What Your Business Owns

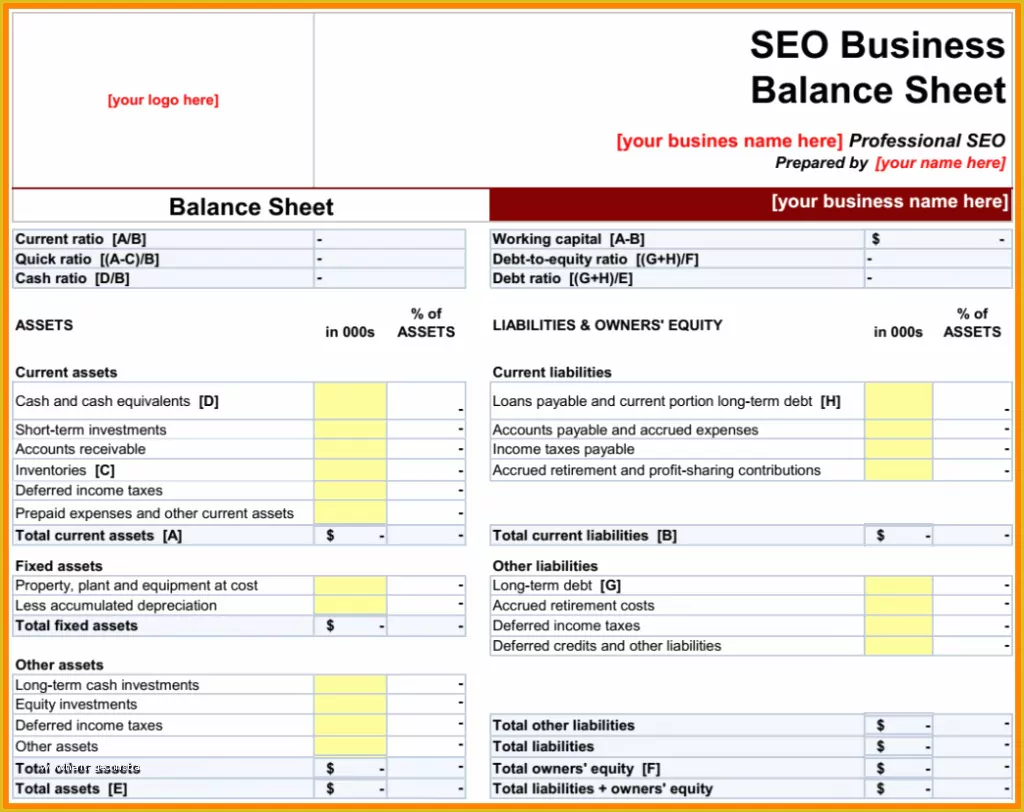

Assets are the economic resources owned by the company that have future economic value. They are what the business uses to operate and generate revenue. Assets are typically listed in order of liquidity, meaning how quickly they can be converted into cash. They are divided into two main categories.

Current Assets are assets that are expected to be converted into cash, sold, or consumed within one year. They are essential for funding day-to-day operations. Key examples include:

* Cash and Cash Equivalents: This is the most liquid asset, including physical currency, bank account balances, and short-term money market funds.

* Accounts Receivable: This is the money owed to your business by customers for goods or services that have been delivered but not yet paid for.

* Inventory: This includes raw materials, work-in-progress, and finished goods that the company plans to sell.

* Prepaid Expenses: These are payments made in advance for future goods or services, such as insurance premiums or rent.

Non-Current Assets (also known as long-term or fixed assets) are resources that are not expected to be converted into cash within one year. They represent the long-term investments of the business. Examples include:

* Property, Plant, and Equipment (PP&E): This includes land, buildings, machinery, vehicles, and furniture. The value of these assets (except land) is reduced over time through a process called depreciation.

* Intangible Assets: These are non-physical assets that still have value, such as patents, trademarks, copyrights, and goodwill.

* Long-Term Investments: These could include stocks, bonds, or real estate held for more than a year.

Liabilities: What Your Business Owes

Liabilities represent the financial obligations or debts of the company to other parties. They are the claims that creditors have on the company's assets. Like assets, liabilities are categorized based on their due date.

Current Liabilities are debts that are due within one year. Managing these is crucial for maintaining short-term financial health. Common examples are:

* Accounts Payable: This is the money your business owes to its suppliers or vendors for goods and services purchased on credit.

* Short-Term Loans: This includes any debt that must be repaid within the next 12 months.

* Accrued Expenses: These are expenses that have been incurred but not yet paid, such as employee salaries, wages, or taxes.

* Unearned Revenue: This is money received from a customer for a product or service that has not yet been delivered.

Non-Current Liabilities (or long-term liabilities) are obligations that are due more than one year from the date of the balance sheet. They are typically used to finance long-term assets. Examples include:

* Long-Term Loans: This includes business loans, mortgages, or other forms of debt with a repayment period extending beyond one year.

* Bonds Payable: If the company has issued bonds to raise capital, the principal amount is a long-term liability.

* Deferred Tax Liabilities: These are taxes that are owed but will not be paid within the current year.

Owner's Equity: The Net Worth of Your Business

Owner's Equity, also known as Shareholder's Equity for corporations, represents the net worth of the company. It is the residual amount left over for the owners after all liabilities have been subtracted from all assets (Equity = Assets - Liabilities). It essentially signifies the owners' stake in the company.

The main components of owner's equity are:

* Paid-in Capital: This is the amount of money invested in the business by its owners or shareholders in exchange for stock.

* Retained Earnings: This is the cumulative net income of the business that has been reinvested in the company and not paid out to owners as dividends. A positive retained earnings figure indicates profitability over time.

How to Fill Out Your Business Plan Balance Sheet Template

With a clear understanding of the components, you can confidently begin to populate your template. Following a structured process ensures accuracy and prevents the final numbers from being a frustrating puzzle.

Step 1: Gather Your Financial Data

Before you can enter any numbers, you need to collect all relevant financial documents. This is the most crucial step, as the accuracy of your balance sheet depends entirely on the quality of your source data. You will need:

* Bank and cash statements for cash balances.

* Inventory records detailing the value of your stock.

* An accounts receivable aging report showing what customers owe you.

* An accounts payable aging report showing what you owe suppliers.

* Loan agreements and statements for all short-term and long-term debt.

* Fixed asset records, including purchase prices and depreciation schedules.

* Records of owner investments and any distributions (dividends).

Step 2: List and Total Your Assets

Start with the asset side of the template. Systematically list each asset under the correct category—current or non-current. For each item, enter its value as of the balance sheet date. For example, list your cash on hand, calculate the total of your accounts receivable, and determine the value of your inventory. For fixed assets like equipment, list the original cost and subtract any accumulated depreciation to find its current book value. Once all individual assets are listed, sum them to get your Total Assets.

Step 3: List and Total Your Liabilities

Move to the liabilities section. Just as with assets, list each liability under the appropriate current or non-current heading. Input the amount owed for accounts payable, the outstanding balance on short-term loans, and any accrued expenses. Then, list the principal amounts for all long-term debts. Sum these figures to arrive at your Total Liabilities.

Step 4: Calculate Your Owner's Equity

Calculate the components of your owner's equity. List the total capital contributed by owners since the business started. Then, calculate your retained earnings. This is typically your cumulative net income from all previous periods, minus any dividends paid out to owners. Sum these amounts to find your Total Owner's Equity.

Step 5: Verify the Accounting Equation

This is the moment of truth. Add your Total Liabilities and your Total Owner's Equity together. This sum must equal your Total Assets.

* Assets = Liabilities + Owner's Equity

If the two sides match, your balance sheet is in balance. If they don't, you need to troubleshoot. Common errors include data entry mistakes, misclassifying an asset as a liability (or vice versa), or errors in depreciation or retained earnings calculations. Methodically re-check your source documents and calculations until the equation balances.

Common Mistakes to Avoid When Using a Balance Sheet Template

Using a template simplifies the process, but it doesn't eliminate the potential for errors. Being aware of common pitfalls can save you time and ensure your financial statements are credible.

- Mixing Personal and Business Finances: This is a cardinal sin for any business owner. Always maintain separate bank accounts and records. Mingling funds makes it nearly impossible to create an accurate balance sheet and can lead to serious legal and tax complications.

- Inaccurate Asset Valuation: It's easy to overstate or understate the value of assets. Inventory should be valued at its cost or its current market value, whichever is lower. Fixed assets must be recorded at their historical cost less accumulated depreciation, not their perceived resale value.

- Forgetting Accruals and Payables: Small business owners often operate on a cash basis and can forget to include expenses that have been incurred but not yet paid (accrued expenses) or bills from suppliers (accounts payable). These are legitimate liabilities and must be included.

- Ignoring Depreciation: Failing to account for the depreciation of fixed assets overstates their value and, consequently, the company's total assets and equity. Use a consistent depreciation method (e.g., straight-line) to systematically reduce the book value of your tangible assets over their useful life.

- Using a Single, Static Balance Sheet: A balance sheet is a snapshot. For a business plan, investors want to see progress. You should create pro forma, or projected, balance sheets for the next three to five years. This shows how you expect the company's financial position to evolve as you execute your plan.

Analyzing Your Balance Sheet: What the Numbers Tell You

A completed balance sheet is more than a list of numbers; it's a rich source of information about your company's financial health. By calculating a few key financial ratios, you can unlock powerful insights.

Liquidity Ratios

Liquidity ratios measure a company's ability to meet its short-term obligations (those due within one year). They answer the question: "Can we pay our upcoming bills?"

- Current Ratio: Calculated as Current Assets / Current Liabilities. A ratio greater than 1 suggests the company has enough short-term assets to cover its short-term debts. A ratio of 2:1 is often considered healthy, but this varies by industry.

- Quick Ratio (Acid-Test Ratio): Calculated as (Current Assets - Inventory) / Current Liabilities. This is a more conservative measure of liquidity because inventory can sometimes be difficult to sell quickly. It shows a company's ability to pay its current liabilities without relying on the sale of inventory.

Solvency Ratios

Solvency ratios measure a company's ability to meet its long-term debt obligations. They assess the long-term financial viability of the business.

- Debt-to-Equity Ratio: Calculated as Total Liabilities / Owner's Equity. This ratio indicates how much debt a company is using to finance its assets relative to the amount of value represented in owners' equity. A high ratio suggests higher risk and heavy reliance on debt financing.

- Debt-to-Asset Ratio: Calculated as Total Liabilities / Total Assets. This ratio shows the proportion of a company's assets that are financed through debt. A ratio greater than 1 means the company has more debt than assets, which is a sign of significant financial risk.

Finding the Right Business Plan Balance Sheet Template

You don't need to create a balance sheet from scratch. Numerous templates and tools are available to help you structure your financial data correctly.

- Spreadsheet Software (Excel, Google Sheets): This is the most common and flexible option. You can find countless free templates online that can be easily downloaded and customized. The major benefit is control, but the downside is that you are responsible for all formulas and data entry, increasing the risk of manual errors.

- Accounting Software (QuickBooks, Xero, Wave): If you are already using accounting software to manage your day-to-day bookkeeping, it can generate a balance sheet for you automatically. This is the most accurate method, as the report is created directly from your live financial data.

- Business Plan Software (LivePlan, Bizplan): These dedicated platforms guide you through the entire business planning process. They typically include integrated financial modules where you input your assumptions, and the software automatically generates your balance sheet, income statement, and cash flow statement.

When choosing a template, look for one that is clearly formatted, includes all the standard line items, and has built-in formulas to automatically calculate totals and check that the sheet balances.

Conclusion

The balance sheet is far more than a mandatory document to be tucked away in your business plan. It is a dynamic and revealing portrait of your company's financial foundation. By taking the time to understand its components—assets, liabilities, and equity—you empower yourself to move beyond simply filling in a Business Plan Balance Sheet Template and toward making truly informed strategic decisions. This single document provides clarity on your company's solvency, liquidity, and overall value.

Mastering your balance sheet builds confidence, both for you as a business owner and for the investors and lenders you seek to attract. It demonstrates a command of your company's financial realities and your preparedness for the challenges ahead. Whether you use a simple spreadsheet or sophisticated software, the principles remain the same. Embrace the balance sheet not as a chore, but as an essential compass guiding your business toward a stable and prosperous future.

0 Response to "Master Your Business Plan Balance Sheet Template"

Posting Komentar